Do SMEs Really Need Sustainability Reporting? (When to Start and When to Wait?)

Sustainability reporting is often associated with large, listed companies. For many SMEs, the assumption is simple: “This doesn’t apply to us.” In reality, sustainability reporting does not start when regulation kicks in. For SMEs, it usually begins much earlier when a major customer demands it, a bank asks for it during a loan application, or when it becomes a mandatory tender requirement.

This article helps SMEs distinguish between when sustainability reporting becomes a business necessity and when it can safely wait.

When SMEs Do NOT need sustainability reporting (yet)

Not every SME needs a sustainability report immediately. If your business falls into the following categories, formal reporting is likely optional for now:

- Hyper-Local: You operate locally with no large corporate or multinational customers.

- Self-Funded: You are not seeking external bank financing or green loans.

- No Tenders: You do not participate in government or large corporate tenders.

- Minimal Direct Impact: Your business has minimal direct emissions and waste, operates in a lightly regulated sector, and faces limited ESG risk beyond standard workforce, data protection, and governance practices.

In these situations, your focus should be on internal awareness and operational efficiency rather than public disclosures.

The Real Triggers: When it Becomes a Business Risk

For most growing SMEs, the “trigger” to start reporting is not a new regulation, but a commercial pressure point. Reporting becomes necessary when one of these four shifts occurs:

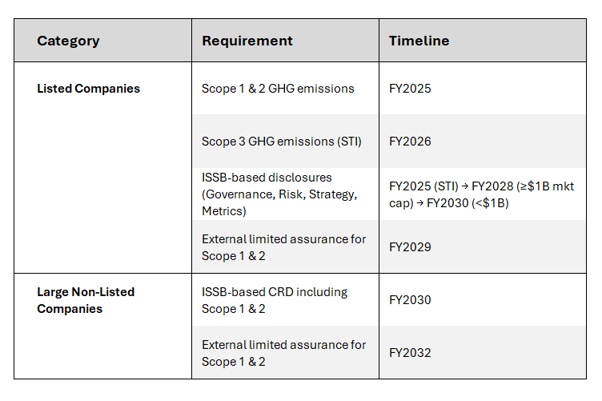

1. Customer or supply-chain pressure – Large listed companies are now required to report their Scope 3 (supply chain) emissions. This means they need your data to complete their report.

- The Reality: Suppliers who can provide accurate carbon data are becoming preferred partners. Those who cannot are risking vendor delisting.

2. Access to Capital (Green Loans) – Banks are increasingly embedding sustainability criteria into credit risk assessments.

- The Reality: Even basic disclosures can unlock green or sustainability-linked financing rates or ensure your credit facility is renewed without friction.

3. Investor Due Diligence – Private equity and strategic partners now routinely ask for “ESG visibility” during due diligence.

- The Reality: A lack of data is often viewed as a lack of governance risk management.

4. Regulatory spillover – While regulations may not apply directly to SMEs yet, compliance requirements for larger companies often flow downstream. SMEs are increasingly asked to align policies, data, and controls to meet their customers’ regulatory obligations, and this request often comes with short notice.

What a Sustainability Report Is (and Is Not)

A sustainability report is often misunderstood as a compliance exercise or a marketing brochure. It is neither. At its core, it is a strategic tool that explains how your business creates long-term value while managing its Environmental, Social, and Governance (ESG) risks. It serves four key commercial purposes that go beyond “saving the planet”:

- Build Trust and Credibility: It provides transparent, structured information that customers, banks, investors, and partners can rely on; moving you beyond vague marketing claims.

- Support Better Decision-Making: By tracking ESG data (energy, workforce, governance), management gains clearer insight into operational risks, inefficiencies, and cost-saving opportunities.

- Demonstrate Resilience: It proves to stakeholders that you can identify and manage risks, from climate disruptions to supply chain gaps, that could affect your business continuity.

- Enable Access to Opportunities: Many commercial doors such as tenders, financing, partnerships and grants; now require some level of ESG disclosure. Reporting helps you walk through them credibly.

Credibility over Perfection

This brings us to a crucial point: Sustainability reporting is not about being “perfect” or looking “green”. We often see SMEs delay reporting because they feel they are not “sustainable enough” yet. This is a strategic mistake. Stakeholders do not expect you to be zero-carbon overnight; they expect you to be honest and in control.

Reporting is a management tool, not a PR exercise. Even if your numbers are not perfect today, disclosing them shows that management is measuring its non-financial risks and has a plan for progress. That transparency builds far more trust than silence.

Summary: When to Start?

An SME should consider starting sustainability reporting when:

- It protects a key customer relationship

- It unlocks cheaper or easier financing

- It formalises internal data and accountability

- It positions the company for a future exit or investment

Starting early, at a manageable scale, is far cheaper than rushing to comply during a tender deadline.

Preparing your first sustainability report?

Don’t guess. Start with the fundamentals :

- Clear Scope

- Defensible Data

- Defined Ownership

Related Resource: Our First Sustainability Report